Should investors steer clear of Tesla shares?

Any investment in the motor industry comes with a severe risk warning currently, but analyst Rodney Hobson still rates one big manufacturer a buy. Another is a wild punt by anyone’s reckoning.

2nd April 2025 07:55

Investors have quite reasonably taken the view that US President Donald Trump’s tariffs will hurt vehicle makers in America and Europe as much as any sector. It seems that even American car makers who are supposed to benefit have similar doubts. And the President is keeping us guessing.

Trump’s grasp on reality is a big imponderable. He claims he “couldn’t care less” if carmakers raise prices in the United States after his proposed 25% tariffs on foreign-made vehicles come into effect. He hopes that when foreign carmakers are forced to raise prices it will persuade Americans to buy American-made cars.

- Invest with ii: Buy US Stocks from UK | Most-traded US Stocks | Cashback Offers

In theory this should indeed help American carmakers as they will be able to raise their own prices, fattening profit margins, while still undercutting foreign imports. In reality, American manufacturers will see their costs rise as parts imported from Canada and Mexico suffer from these tariffs. Even worse, car production could be disrupted, leading to temporary shutdowns and negating Trump’s boast that “we have plenty” of American-made cars.

Meanwhile Canada, the European Union and the UK are threatening retaliatory tariffs against American cars. In addition, there is growing ill feeling in Europe towards vehicles shipped from across the Atlantic. The European Automobile Manufacturers Association reported that new registrations of cars made by Tesla Inc (NASDAQ:TSLA) dropped 40% in February despite a 26% increase in electric vehicle registrations overall. Tesla’s share of the European market slumped from 2.8% to 1.8%.

It is now three weeks since Tesla wrote to US Trade Representative Jamieson Greer warning that American exporters were "exposed to disproportionate impacts when other countries respond to US trade actions".

- Q1 Wall Street review: big losses and Liberation Day gossip

- Tariffs: how to shield your portfolio from uncertainty and fund pick

Tesla’s chief, in case anyone has forgotten, is White House favourite Elon Musk. If his company cannot influence the president, one must assume that Trump is dead set on his course of action.

It is therefore difficult to see any way in which the immediate future is bright for vehicle manufacturers anywhere.

Tesla shares were a grossly overvalued $480 in mid-December; they halved to $222 before stabilising for the time being at around $260. Even with that drop, the price/earnings (PE) ratio is still a hefty 130.

Source: interactive investor. Past performance is not a guide to future performance.

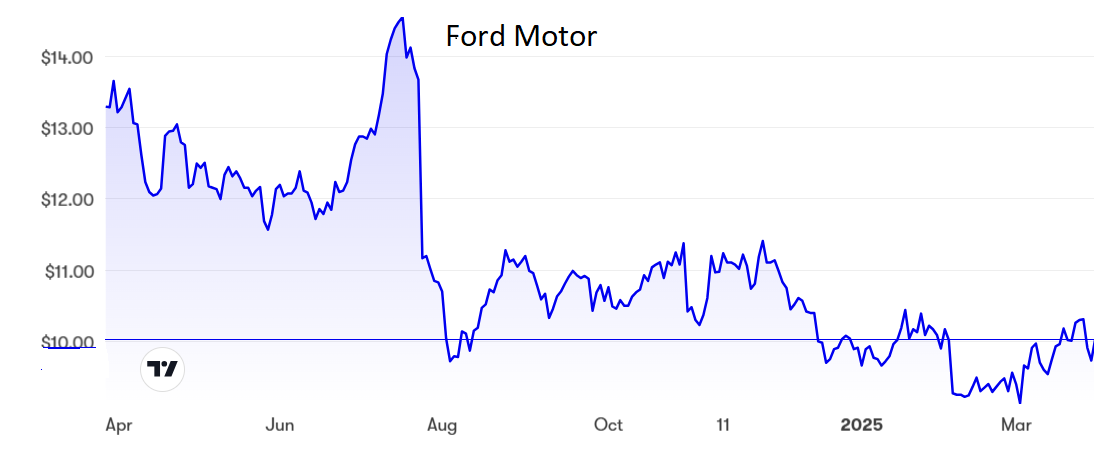

Ford Motor Co (NYSE:F) shares have actually stabilised since falling from $14.50 to $9 last summer. At the current $10 it has the rare distinction of having a yield (7.7%) that is larger than its PE (6.7).

Source: interactive investor. Past performance is not a guide to future performance.

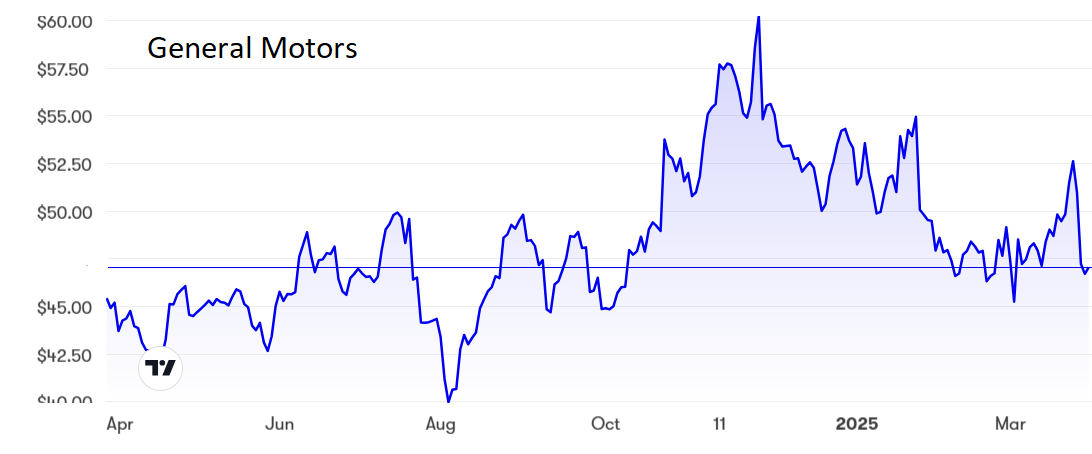

General Motors Co (NYSE:GM) peaked at $60 in November but is now down to $47, where the PE is 7.3 but the yield is only just above 1%.

Source: interactive investor. Past performance is not a guide to future performance.

However, it is European manufacturers who are likely to suffer most. Vehicles from the European Union account for 21% of such imports into the US. German makers will be most affected, especially Volkswagen AG (XETRA:VOW), where shares have slipped from €112 in mid-March to under €100. The yield at 9% is almost double the PE at 4.65, an extraordinary state of affairs that assumes earnings and the dividend will both be slashed soon.

Source: interactive investor. Past performance is not a guide to future performance.

Hobson’s choice: Any investment in vehicle manufacturers in the United States or Europe at this stage must come with a very obvious severe risk warning. Even those investors with an appetite for risk may feel it is wise to hold off for now and await developments, although that means possibly missing out if the tariff war is unexpectedly resolved.

Stay well clear of Tesla. Its shares are still seriously overvalued. My December buy rating on Ford still stands despite the tariff turmoil. The rating allows for a lot of bad news and the dividend provides some comfort. I suggested that General Motors was also still a buy in December, but the tariff war has had more impact on its share price than at Ford. There could be more pain to come but the shares are worth holding on to if you are a holder.

Volkswagen is a wild punt by anyone’s reckoning but if you are already in it is probably worth holding on, although you may feel you have suffered enough pain already.

Rodney Hobson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.

Editor's Picks