Shares for the future: here’s how I rank this simple AIM stock

Its founder believes his company is so simple that it should be able to run itself. Analyst Richard Beddard shares his view on the business after meeting the man himself.

4th April 2025 14:42

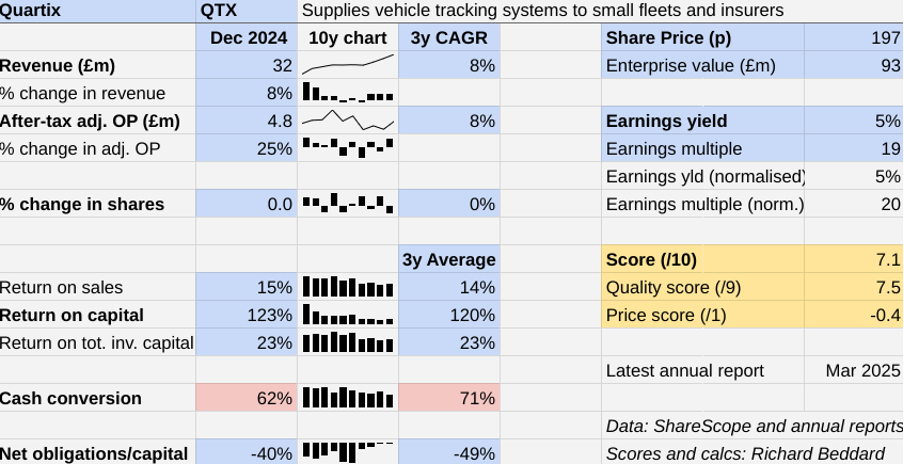

Vehicle tracking firm Quartix Technologies (LSE:QTX) may have turned a corner in the year to December.

I met the company’s founder, Andy Walters, after the AGM earlier this week to find out more about a wayward couple of years that prompted him to return to the business in 2023 and 2024, and the steps he is taking to get it back on track.

He retired in 2021.

- Invest with ii: Open an ISA | ISA Investment Ideas | Transfer a Stocks & Shares ISA

Scoring Quartix: back in the driving seat

Revenue grew 8%, and after-tax adjusted operating profit grew 25% in 2024, albeit compared to one of the worst years in the company’s recent history.

The Past (dependable) [2.5]

- Profitable growth: Profit is lower than it was in 2018 [0.5]

- Strong finances: Net cash [1]

- Through thick and thin: Lowest RoC: 112% (2023) [1]

My table focuses on the last three years because the business was changing shape before 2022 as it wound down sales of tracking devices to insurers. By 2022, the division was so small, Quartix stopped reporting its performance.

The company is now focused on its fleet business, which has been earning recurring revenues from commercial van operators since it was founded in 2001.

To grow this business, Quartix has increased investment in sales and marketing to acquire new customers overseas. It first targeted France in 2010 and has an established business there. More recently, it has entered other European markets and the US.

The cost of international expansion has been joined over the last three years by inflation in component and staff costs, and a decision to invest in a new product that went nowhere.

The diworsification was Quartix EVolve, a tool designed to help fleet operators decide which electric vehicles to buy based on their tracking data. Adding to costs in 2023, Quartix acquired Konetik, the company that wrote the EVolve software, to prevent it going into liquidation.

- When markets fall, here’s what to avoid doing

- A decade of pension freedoms: what you’ve done with your money

Soon after the acquisition, Andy Walters returned. He discontinued EVolve, liquidated Konetik, refocused on tracking devices, reduced the size and cost of the board, and for the first time increased prices for existing customers.

This elevated profit in 2024, but despite revenue growth, adjusted profit is still 23% below its peak in 2018.

Cash conversion fell to a sub-par 61% due to the replacement of redundant 2G trackers with 4G units at no cost to the customer. The older units are obsolete due to the retirement of 2G networks in France and the US.

A 12% increase in annualised recurring revenue (ARR) in 2024 bodes well for 2025, when Quartix anticipates low double-digit revenue growth.

It will be reporting an update for the first quarter of 2025 on Monday.

The Present (distinctive) [2.5]

- Discernible business: Reliable tracking for small fleets [1]

- With experienced people: Founder on board, no succession plan [0.5]

- That creates value for customers: Low cost, easy buy, install and use [1]

Quartix supplies a vehicle tracking service powered by small inexpensive devices secured under the bonnet of a van or on its dashboard.

The Printed Circuit Boards are made in China and assembled into tracking devices in the UK. They are typically installed in fleets belonging to trades such as building firms, landscapers and electricians.

The devices relay the vehicle’s position to Quartix’s cloud-based software via mobile networks so owners can monitor fleets in real time on a computer or mobile app. This helps them prevent moonlighting, route drivers to jobs, and ensure vehicles are driven safely and economically.

Almost all Quartix’s income is recurring revenue from data subscriptions sold directly to small businesses via price comparison sites, by telephone, through distributors and, in its larger markets, some field sales people.

More than most companies, Quartix’s development has been guided by one person: Andy Walters. His mantra is to keep things simple.

Simplicity comes in many forms: a generic device that is so easy to install nearly 50% of customers do it themselves, straightforward contracts with no upfront costs that typically require only a one-year commitment, easily configurable software, and centralised support functions.

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

- Insider: more buying as SpaceX firm trades near 17-year high

Mr Walters believes the company he created is so simple, it should be able to run itself. He appears to be trying to make himself almost redundant.

His return in late 2023 triggered a boardroom clear out. The chief executive, the chief financial officer, and all three non-executives, had gone by March 2024.

Today, a board of three runs the company, two new non-executive directors and the executive chair, who is only committed to eight days work a month.

I wonder about the sustainability of this. Quartix is run by an operating board of trusted long-serving employees, which gives me confidence, but recent events show that the executive chair serves a function: to keep the company on the straight and narrow.

Three things are clear. Mr Walters wants to reduce his workload below his eight-day commitment, although he is currently working more. He has no plans to beef up the PLC board. And he has no plans to step down from the board again, while he remains a major shareholder.

The Future (directed) [2.5]

- Addressing challenges: Cost increases, attrition, UK 2G sunset [0.5]

- With coherent actions: Simplification, expansion, price increases [1]

- That reward all stakeholders fairly: Dedicated management, satisfied customers [1]

Quartix believes it can create large installed bases in Germany, Italy, Spain and the US, and continue to grow the substantial installed bases it already has in the UK and France. Except for the US, revenue growth rates in 2024 were impressive.

In the US, Quartix has reversed previous management’s decision to focus its US expansion on field sales in Texas. This policy contrasted strongly with Quartix’s nationwide and predominantly direct sales model in other countries, and sales contracted. It is early days, but the territory returned to modest revenue growth in 2024.

The biggest challenge facing the business is competition, so much so that until 2024 Quartix had never increased the subscription cost for existing subscribers for fear of losing them.

Quartix says post-pandemic inflation changed that taboo. We have grown used to price increases for subscription products. It does not believe it has lost subscribers due to its first price increase last year.

One year is not much to go on, but Quartix may now have two levers to increase revenue: growing the installed base and annual price increases levied on that installed base. Growth in the installed base depends on Quartix being able to sell new subscriptions faster than customers switch to rivals.

To measure how successfully it manages these levers, Quartix has introduced a new performance indicator: Net Revenue Retention.

At the end of 2024, Quartix had retained 95.7% of the ARR from its subscription base at the beginning of the year. It wants to achieve 100% Net Revenue Retention. This would mean revenue is maintained despite the inevitable loss of subscriptions, even if the company added no new ones.

The company is more circumspect about attrition. The price rise in 2024 concealed an increase in attrition. By my calculation fleet gross attrition, the number the company has substituted with Net Revenue Retention, has increased from 13.3% to 14.5% in 2024.

At one time, Quartix’s attrition rate was as low as 10%, suggesting a typical unit saw 10 years of service. If 2024 is anything to go by, it is more like seven years, today.

In some ways, the industry is a victim of its own success. By making the devices so easy to buy and install, Quartix and its rivals have made it easy for customers to swap.

This means the pressure on price when Quartix is acquiring new customers is as intense, if not more so, than ever. To improve profitability, the company must reduce costs. Except during the brief interregnum in Andy Walters’ leadership, this has always been Quartix’s strong suit.

In addition to refocusing the business in 2024, the company re-engineered the device’s hardware and firmware, which it says has resulted in savings of £8 per unit (a reduction of 20% or so).

- Last-minute ISA ideas for investors looking to ‘buy low’

- Can Africa replicate Asian economic miracle?

These new units will go into production once the existing stock is exhausted this summer, and they will reduce the cost of the upgrade programme in France too.

Quartix is also reviewing its sales channels. Price comparison sites are the most convenient channel, especially in new markets, but telesales is the most profitable and reduces Quartix’s dependence on third parties for leads.

For some time, Quartix has been supplying new customers with 4G devices. Even so, it has a large 2G installed base in the UK that is slowly declining due to attrition, service upgrades and vehicle swaps.

UK network providers have agreed to shut down their networks by 2033, although Quartix’s provider plans to consult customers about a 2030 deadline.

Quartix does not foresee a material upgrade programme, however the French sunsetted their networks earlier than expected. We should not rule out the possibility that it will have to replace substantial numbers of units in the UK, and might choose to do it at its own cost, at some point.

Last year, I misinterpreted a statistic that encouraged me to lop half a point from Quartix’s score. The company reported 31% voluntary employee turnover, which is extraordinarily high. In fact, this statistic was the proportion of leavers that left voluntarily, not the proportion of the total number of employees that left voluntarily, as I thought.

This year’s number, 18%, is the more common version of the statistic. I cannot deny that I would be reassured if it were lower but also recognise that many of Quartix’s employees work in a call centre, and this may not be a permanent career choice for them.

I believe Quartix is good for stakeholders. Apart from the shareholding and singular purpose of its executive chair, which aligns him with shareholders, I have inferred this from its operating board of eight, its most senior employees have combined service of nearly 90 years, and its high Trustpilot score of 4.8.

The price (discounted?) [-0.4]

- No. A share price of 197p values the enterprise at about £93 million, 20 times normalised profit.

A score of 7.1 implies Quartix is probably a good long-term investment.

It is ranked 25 out of 40 shares in my Decision Engine.

29 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score 7 or more out of 10 to be good value. Shares that score 5 or 6 out of 10 are probably fairly priced.

Bunzl (LSE:BNZL) has published its annual report and is due to be re-scored.

|

0 |

company |

* |

description |

score |

|

1 |

Manufactures tableware for restaurants and eateries |

10.0 | ||

|

2 |

Supplies kitchens to small builders |

9.3 | ||

|

3 |

Imports and distributes timber and timber products |

9.0 | ||

|

4 |

Makes light fittings for commercial and public buildings, roads, and tunnels |

8.9 | ||

|

5 |

Manufactures pushbuttons and other components for lifts and ATMs |

8.5 | ||

|

6 |

Distributor of protective packaging |

8.4 | ||

|

7 |

Manufacturer of scientific equipment for industry and academia |

8.4 | ||

|

8 |

Whiz bang manufacturer of automated machine tools and robots |

8.3 | ||

|

9 |

Flies holidaymakers to Europe, sells package holidays |

8.3 | ||

|

10 |

Repair and maintenance of rail, road, water, nuclear infrastructure |

8.3 | ||

|

11 |

Sells promotional materials like branded mugs and tee shirts direct |

8.2 | ||

|

12 |

Manufactures computers, battery packs, radios. Distributes components |

8.2 | ||

|

13 |

Manufactures filters and laboratory equipment |

8.0 | ||

|

14 |

Designs recording equipment, loudspeakers, and instruments for musicians |

8.0 | ||

|

15 |

Distributes essential everyday items consumed by organisations |

7.9 | ||

|

16 |

Surveys and distributes public opinion online |

7.8 | ||

|

17 |

Manufactures vinyl flooring for commercial and public spaces |

7.8 | ||

|

18 |

Retailer of furniture and homewares |

7.7 | ||

|

19 |

Operates tenpin bowling and indoor crazy golf centres |

7.6 | ||

|

20 |

Manufactures/retails Warhammer models, licences stories/characters |

7.4 | ||

|

21 |

Sells hardware and software to businesses and the public sector |

7.4 | ||

|

22 |

Manufacturer of ventilation products |

7.3 | ||

|

23 |

Online marketplace for motor vehicles |

7.3 | ||

|

24 |

Manufactures surgical adhesives, sutures, fixation devices and dressings |

7.2 | ||

|

25 |

Quartix |

Supplies vehicle tracking systems to small fleets and insurers |

7.1 | |

|

26 |

Manufactures PEEK, a tough, light and easy to manipulate polymer |

7.0 | ||

|

27 |

Supplies software and services to the transport industry |

7.0 | ||

|

28 |

Sources, processes and develops flavours esp. for soft drinks |

7.0 | ||

|

29 |

Provides automated marketing software as a service |

7.0 | ||

|

30 |

Manufactures natural animal feed additives |

6.9 | ||

|

31 |

Online retailer of domestic appliances and TVs |

6.7 | ||

|

32 |

Acquires and operates small scientific instrument manufacturers |

6.5 | ||

|

33 |

Translates documents and localises software and content for businesses |

6.5 | ||

|

34 |

Publishes books, and digital collections for academics and professionals |

6.3 | ||

|

35 |

Manufactures disinfectants for simple medical instruments and surfaces |

6.2 | ||

|

36 |

Casts and machines steel. Processes minerals for casting jewellery, tyres |

6.0 | ||

|

37 |

Makes marketing and fraud prevention software, sells it as a service |

5.9 | ||

|

38 |

Manufactures military technology, does research and consultancy |

5.7 | ||

|

39 |

Manufactures sports watches and instrumentation |

5.6 | ||

|

40 |

Runs a network of self-employed lawyers |

4.8 |

Scores and stats: Richard Beddard. Data: ShareScope and annual reports

Click on a share's name to see a breakdown of the score (scores may have changed due to movements in share price)

Shares marked with an asterisk (*) have been re-scored, click the asterisk to find out why.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Quartix and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.

Editor's Picks