What’s next for London’s offices?

As London’s office market faces high vacancy rates and declining values, the focus shifts to connectivity and adaptability.

20th May 2025 14:21

Lance Eddis-Finbow from abrdn

The pandemic has had a significant effect on offices. And it has left a lingering question over the sector: what’s next? With vacancy rates in some of London’s submarkets surpassing 20% [1], office attendance barely accounting for half of the working week [2], and values down around 25% over five years [3], the outlook may appear bleak at first glance.

Major global office markets mirror these trends – and, in some cases, are much more severe. For instance, office values in New York have halved over the last five years, and vacancy rates have soared in markets like Sydney, Dublin, Paris and LA. While London is still a globally connected city, it’s not immune to the pandemic-produced shifts in demographics, workplace habits, economic trends, and policy. Indeed, it has pockets of virtually obsolete buildings and eye-watering availability levels. That said, our research shows strong polarisation across London’s submarkets, which suggests segments of the market are still worth exploring.

Four years ago, we developed the FACTS framework (abbreviated from flexibility, amenity, connectivity, technology, and sustainability) to help make sense of the rapidly shifting world of office requirements. Entering its fourth year, FACTS still holds up to today’s requirements, and we are finding that location (connectivity) is driving the conversation.

Commuting trends

Looking at Transport for London (TfL) data, monthly taps at major central London tube stations have plateaued at around 15% below pre-pandemic averages [4]. Two notable exceptions are Bond Street and Tottenham Court Road stations, which benefit from the Crossrail (Elizabeth Line) connection. Increased connectivity from the line helps retail footfall, local amenities, and commuting times. As a result, nearby office rents, values, and vacancies are outperforming the wider London market.

A growing alternative?

Although much improved from the depths of the pandemic, the average employee spends less time in London’s offices at just 2.7 days per week (down from 3.9 days in 2019) [5]. Over roughly the same period, daily cycle trips have increased by around 20%. According to TfL, cycling now accounts for 15% of all commuting trips within central London. This highlights the need for suitable end-of-trip office facilities (such as showers and lockers). Dockless cycle providers, such as Lime and Forest, have also soared in popularity and offer an alternative for commuters. They connect submarkets and accommodate ‘last-mile’ trips. This is exacerbating the breadth between the winners and losers in today’s office markets. Lime bikes can now be found in over 20 cities from Tokyo to Toronto, which links connectivity to a wide range of office markets globally. The need to amplify connectivity as a major factor in office selection, to draw in staff daily and over the long term, is growing. Therefore, those offices that offer high connectivity are now carrying strong momentum.

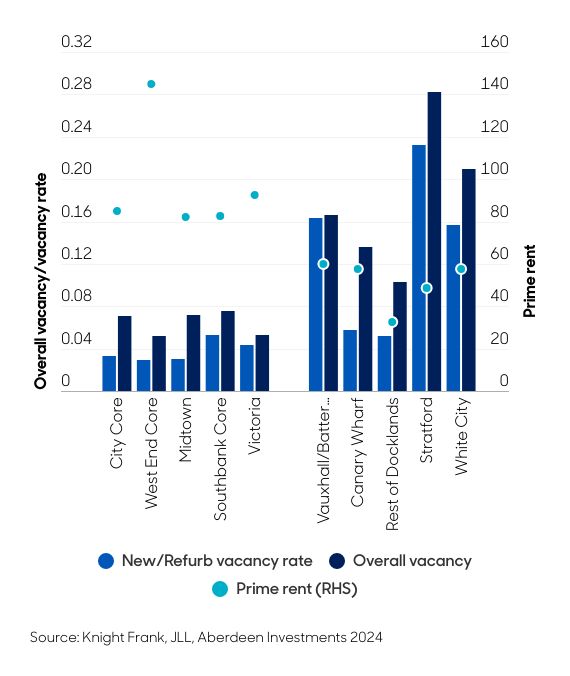

Which offices are performing best?

Core locations within London are outperforming. This is clear when looking at prime rents and vacancy rates across the inner zones of 1-2, versus more peripheral markets. In these less-favourable markets, even new and refurbished space is struggling. These buildings see far less competition, as a result.

West End

Prime rents in the West End have outpaced every other submarket, with a 6.3% annualised uplift over the past five years, according to JLL [7]. Vacancy rates (particularly for new space) are among the lowest in the city, and local development restrictions will keep its already shrinking construction pipeline subdued. In the favoured micro-markets around Mayfair and St. James’s, rents for prime space are above £150 per square foot – a lack of future development will only push up rents until some affordability ceiling is reached. As a result of these demand dynamics, values have held up better and prime yields have proven much steadier against rising interest rates.

The City of London

The development market in the City is undoubtedly more responsive than in the West End, given its more forgiving planning environment. This is good for large-scale developers who are looking to fill a city block with a tower. It’s also good for occupiers who are searching for more space. But both of these factors are proving tough at the moment, as construction and financing costs have halted big projects. As the last of the pandemic-era developments complete during this year, the construction pipeline will drop off. Like the West End, we expect rental growth (which has been a healthy 3.7% annualised over the last five years, according to JLL [8]) to forge ahead in the City, led by top-quality space that’s close to the main transport hubs. When interest rates fall further, we expect yields to fall in the City office market.

Final thoughts…

Within these favoured submarkets, there will be pockets of strong outperformance, owing to the outlined supply/demand imbalances. According to the latest MSCI data, average office values appear to be finding a floor. Additional factors, like energy performance certificate (EPC)-driven obsolescence will drive more occupiers to FACTS-compliant space. Given a lack of future space, and consistent demand for well-located offices, we see this as an attractive entry point for investors who are willing to take on some project risk in select submarkets. London is at the forefront of the office story, but we’ll be looking for clues in other locations, particularly where we see brightly coloured dockless bikes popping up.

Lance Eddis-Finbow is senior real estate investment analyst at Aberdeen.

-

Knight Frank London Office Spotlight

-

Centre for Cities – link: https://www.centreforcities.org/reader/return-to-the-office/

-

MSCI Quarterly Index data

-

Transport for London open data

-

Centre for Cities – link: <a href="https://www.centreforcities.org/reader/return-to-the-office/">Return to the office | Centre for Cities</a>

-

Knight Frank Offices Spotlight Q3 2024

-

JLL subscription data

-

JLL subscription data

ii is an Aberdeen business.

Aberdeen is a global investment company that helps customers plan, save and invest for their future.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Editor's Picks