Still time to buy into these two tech winners

These companies have deep pockets, so can shoulder the investment needed to keep ahead of the game. Analyst Rodney Hobson examines their potential following strong second-quarter earnings.

6th August 2025 10:31

Big American tech companies are really on a roll, with a series of sparkling second-quarter results that beat analysts’ expectations. Share prices are admittedly looking pretty rich but this is by no means a repeat of the tech boom and bust that marked the millennium, when technology was in its infancy.

A quarter of a century on, even the virtual reality is really here. So, like it or loathe it, is artificial intelligence (AI), and cloud computing is pervasive. Put AI and cloud computing together and there’s plenty of fast-growing business to go round all the major players.

- Invest with ii: Buy US Stocks & Shares | US Earnings Season | Interactive investor Offers

Competition regulators may chafe over the stranglehold that big tech companies have on their markets but the exponential growth of information technology means competitors will find it increasingly difficult – and expensive – to break in. Big tech have the financial and legal resources to stand their ground and the occasional financial penalty is peanuts compared with what they earn.

These companies can also stand the hefty investment needed to keep ahead of the game. For example Meta Platforms Inc Class A (NASDAQ:META) is reckoning on splashing out about $70 billion (£53 billion) in capital spending this year, roughly double what it allocated in 2024; Microsoft Corp (NASDAQ:MSFT) shelled out $24 billion in the second quarter alone. Increased advertising revenue is funding the merry-go-round.

- AI demand generates ‘phenomenal’ quarter for tech firm

- Two legendary tech stocks moving with the times that rate a buy

What they may have difficulty with is finding the computer whizz-kids to develop the current phase of highly sophisticated technology. Meta has paid $14.3 billion for a stake in ScaleAI, not so much because it wants to take over a company that is little more than a start-up but because it wants ScaleAI’s 28-year-old chief executive Alexandr Wang onside. Meta has also poached researchers from AI rivals with massive pay packages.

Source: interactive investor. Past performance is not a guide to future performance.

Yet the potential for revenue and profits is also colossal. Meta reported net income up 36% to $18.3 billion on revenue 22% higher at nearly $40 billion, a good 6% more than was expected. Chief executive Mark Zuckerberg now reckons revenue could hit $50 billion in the current three months, although with a slowdown in growth in the fourth quarter.

Even so, Meta, the owner of social media sites Facebook and Instagram, has some catching up to do with competitors such as Amazon.com Inc (NASDAQ:AMZN) and Google owner Alphabet Inc Class A (NASDAQ:GOOGL) in building AI infrastructure and software.

Microsoft pointed to a great performance by its Azure cloud business, which incorporates AI tools, as it reported net income up 24% to $27.2 billion on revenue 18% higher at $76.4 billion, about $2.5 billion more than the average forecast.

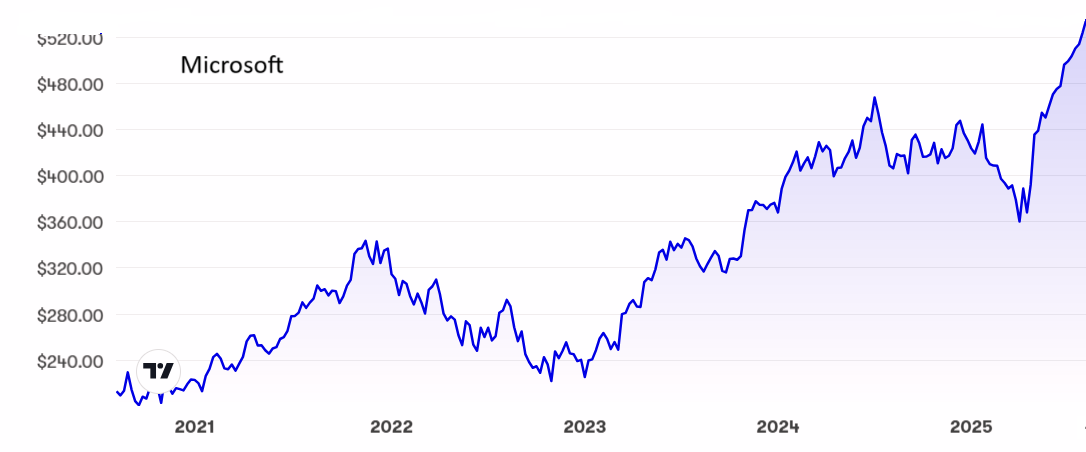

Source: interactive investor. Past performance is not a guide to future performance.

Revenue over the past 12 months was 15% higher at $282 billion and net income 16% up at $128.5 billion, which implies some acceleration in growth in the latest quarter compared with the previous nine months.

Microsoft is already leading the way in making money from AI. It has exclusive access to Open-AI technology, which is attracting customers to its cloud computing service as new products are quickly rolled out.

- Don’t chase AI – back the companies using it best

- Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

Shares in both companies jumped immediately on the figures, Meta by 8% and Microsoft 7%. Meta hit a peak at $779, having bottomed at $500 in April, and is now trading at $765. The price/earnings (PE) ratio is still only 27, which does not reflect the projected meteoric growth. Amazingly for a company that needs to keep investing, there’s actually a paltry dividend.

Microsoft’s chart tells a similar story as it bounced up from $360 in April to a new peak of $535 before settling just under $530 now. The PE is a little more challenging at 38, but the yield is slightly better at 0.6%.

Hobson’s choice: I recommended Meta below $300 in August 2023 and again just above $700 in February this year. The upward momentum is set to continue. Meta and Microsoft are still a buy.

Rodney Hobson is a freelance contributor and not a direct employee of interactive investor.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.

Editor's Picks